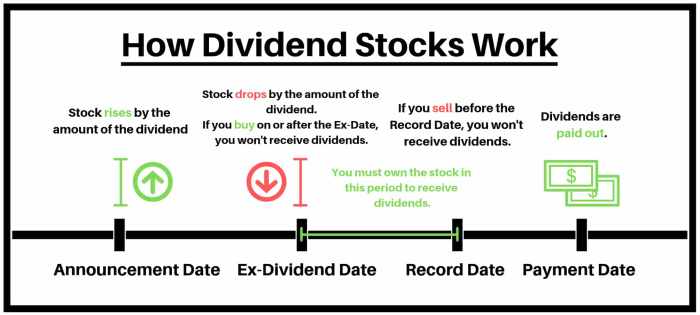

The allure of passive income, a steady stream of financial reward without constant active effort, has captivated investors for generations. Dividend investing, a cornerstone of this pursuit, offers a compelling path to financial freedom. By strategically selecting companies that distribute a portion of their profits to shareholders, investors can generate a consistent income stream, supplementing their existing earnings or providing a foundation for retirement.

This approach, however, requires a careful understanding of financial markets, risk assessment, and tax implications. This exploration delves into the intricacies of dividend investing, navigating the complexities and illuminating the potential rewards.

Understanding dividend investing involves recognizing that it’s not a get-rich-quick scheme but rather a long-term strategy requiring patience and informed decision-making. The process encompasses selecting suitable dividend-paying assets—from individual stocks and Real Estate Investment Trusts (REITs) to diversified Exchange-Traded Funds (ETFs)—each carrying its own unique risk profile and potential return. Effective portfolio diversification, coupled with a robust understanding of dividend reinvestment plans (DRIPs) and tax implications, forms the bedrock of successful dividend investing.

This detailed analysis will equip you with the knowledge to navigate these complexities and build a resilient, income-generating portfolio.

Introduction to Dividend Investing

Dividend investing represents a compelling passive income strategy, allowing investors to generate a consistent stream of income from their investments. Unlike strategies focused solely on capital appreciation, dividend investing prioritizes the receipt of regular dividend payments from companies that distribute a portion of their profits to shareholders. This approach can be particularly attractive to investors seeking a reliable income stream, supplementing other sources of retirement income, or building wealth gradually over time.

The core principle lies in owning shares of companies with a proven track record of distributing dividends, thereby generating a passive income stream while potentially benefiting from long-term capital appreciation.Dividend investing, like any investment strategy, presents both advantages and disadvantages. Understanding these aspects is crucial for making informed investment decisions.

Benefits and Risks of Dividend Investing

The benefits of dividend investing include the generation of a consistent income stream, providing financial stability and supplementing other income sources. Furthermore, companies with a history of consistent dividend payments often demonstrate financial strength and stability, implying a lower risk profile compared to companies that do not pay dividends. Reinvesting dividends can accelerate wealth accumulation through the power of compounding returns.

However, dividend investing also carries inherent risks. Dividend payments are not guaranteed; companies can reduce or eliminate dividends during periods of financial distress. Furthermore, the value of dividend-paying assets can fluctuate, impacting the overall return on investment. The income generated from dividends may also be subject to taxation. Finally, dividend yields are not always indicative of future performance; a high yield may signal underlying financial weakness.

Types of Dividend-Paying Assets

Several asset classes offer dividend-paying opportunities.

Common stocks represent fractional ownership in a publicly traded company. Companies distribute dividends based on their profitability and financial policies. For example, a well-established company like Coca-Cola (KO) has a long history of paying dividends, providing a relatively stable income stream for investors. However, the dividend amount can vary based on the company’s performance.

Real Estate Investment Trusts (REITs) are companies that own or finance income-producing real estate. REITs are legally required to distribute a significant portion of their taxable income to shareholders as dividends, making them attractive for income-seeking investors. For instance, a REIT focused on apartment buildings might generate a consistent dividend stream from rental income. However, REIT performance is sensitive to interest rate changes and fluctuations in the real estate market.

Exchange-Traded Funds (ETFs) that focus on dividend-paying stocks offer diversification and convenience. These ETFs pool investments in a basket of dividend-paying stocks, providing exposure to a diversified portfolio with a single investment. A popular example is the Vanguard High Dividend Yield ETF (VYM), which invests in a diversified portfolio of high-dividend-yielding stocks. The diversification reduces the risk associated with individual stock selection, but the overall return depends on the performance of the underlying stocks within the ETF.

Selecting Dividend-Paying Stocks

The selection of dividend-paying stocks forms the cornerstone of a successful passive income strategy. A rigorous and informed approach is crucial, balancing risk tolerance with the potential for consistent returns. This involves understanding key financial metrics and applying a systematic process to identify companies that are likely to deliver sustainable dividend payments over the long term.

Share Criteria for Choosing High-Quality Dividend-Paying Stocks

Choosing high-quality dividend stocks requires a multifaceted approach. Investors should consider a company’s financial health, its history of dividend payments, and the sustainability of its future payouts. A thorough analysis involving several key financial ratios is necessary. For instance, a high dividend yield alone isn’t sufficient; it must be coupled with strong underlying fundamentals.

Dividend Payout Ratios and Their Implications

The dividend payout ratio, calculated as (Dividends per share)/(Earnings per share), represents the proportion of a company’s earnings distributed as dividends. A low payout ratio (e.g., below 50%) suggests the company retains a significant portion of its earnings for reinvestment, fostering growth and potentially supporting future dividend increases. Conversely, a high payout ratio (e.g., above 70%) might indicate a greater reliance on debt or reduced capacity for future growth, increasing the risk of dividend cuts.

However, established, mature companies with stable earnings may maintain high payout ratios without jeopardizing their financial stability. The ideal payout ratio varies depending on the industry, company maturity, and growth prospects. A company with a consistently high payout ratio may be suitable for an investor seeking higher current income, while a lower payout ratio might appeal to those prioritizing long-term growth potential.

Hypothetical Dividend Stock Portfolio

This hypothetical portfolio illustrates a diversified approach to dividend investing, incorporating varying risk profiles. The risk assessment is subjective and depends on individual investor tolerance.

| Stock Name | Dividend Yield | Payout Ratio | Risk Assessment |

|---|---|---|---|

| Johnson & Johnson (JNJ) | 2.8% | 55% | Low |

| Coca-Cola (KO) | 3.2% | 60% | Low to Moderate |

| Real Estate Investment Trust (REIT)

Example Realty Income (O) |

4.5% | 80% | Moderate |

| Energy Company – Example: ExxonMobil (XOM) | 4.0% | 40% | Moderate to High (dependent on oil prices) |

Dividend Reinvestment Plans (DRIPs)

Dividend reinvestment plans, or DRIPs, offer a powerful mechanism for long-term investors to organically grow their portfolios. By automatically reinvesting dividend payments back into the same company’s stock, DRIPs leverage the compounding effect of returns, accelerating wealth accumulation. This strategy minimizes transaction costs and maximizes the benefits of consistent dividend payouts.

DRIPs operate on a straightforward principle: when a company pays a dividend, instead of receiving the cash payment, the investor opts to use that dividend to purchase additional shares of the company’s stock. This purchase is typically executed at a small discount or without brokerage fees, unlike traditional stock purchases. The mechanics often involve the company’s transfer agent handling the reinvestment process.

This automated system removes the need for manual intervention, streamlining the process and making it incredibly convenient for investors.

DRIP Mechanics and Advantages

DRIPs offer several compelling advantages. The most significant is the compounding effect. By reinvesting dividends, investors gain more shares, which, in turn, generate even larger dividends over time. This snowball effect exponentially increases the growth of the investment portfolio. The absence of brokerage commissions further enhances returns.

Each purchase of additional shares through a DRIP typically avoids the usual brokerage fees, leading to significant savings, especially over extended investment horizons. This cost savings translates directly into higher overall returns. Furthermore, DRIPs often allow for fractional share purchases, enabling investors to fully utilize even small dividend payments. This ensures that no portion of the dividend income is wasted.

Tax Implications of DRIPs

While DRIPs offer significant financial benefits, understanding the tax implications is crucial. Dividends received are still taxable income in the year they are received, regardless of whether they are reinvested. The IRS treats the dividend reinvestment as a taxable event. Therefore, investors should adjust their tax withholding or make estimated tax payments to account for these dividend payments.

The tax implications are identical to receiving the dividend in cash and then purchasing additional shares separately. The key difference lies in the convenience and cost savings associated with the DRIP program itself, which doesn’t change the tax treatment of the dividend income. Accurate record-keeping is paramount for efficient tax filing.

Enrolling in a DRIP: A Step-by-Step Guide

Participating in a DRIP is generally a straightforward process. However, the specific steps might vary slightly depending on the company and its transfer agent.

The following steps provide a general overview of the enrollment process:

- Locate the DRIP Information: Check the company’s investor relations section on its website. This section typically contains details about the DRIP program, including enrollment forms and contact information for the transfer agent.

- Complete the Enrollment Form: Carefully fill out the enrollment form, providing all necessary information, including your brokerage account details (if applicable) and your preferred method of reinvestment (e.g., automatic reinvestment of all dividends or a partial reinvestment option).

- Submit the Enrollment Form: Submit the completed enrollment form according to the instructions provided. This usually involves mailing the form to the designated transfer agent address.

- Initial Investment (Optional): Some DRIPs may require an initial investment to enroll. Check the enrollment materials for specific requirements.

- Monitor Your Account: Once enrolled, regularly monitor your account to track the growth of your investment and ensure that dividends are being reinvested correctly.

Building a Diversified Dividend Portfolio

Diversification is a cornerstone of successful long-term dividend investing. It mitigates risk by spreading investments across various asset classes, sectors, and geographies. This approach reduces the impact of any single investment’s underperformance on the overall portfolio’s return and dividend income stream. A well-diversified portfolio aims to balance risk and reward, maximizing potential returns while minimizing the likelihood of significant losses.The principle of diversification rests on the statistical concept of reducing portfolio variance.

By combining assets with low or negative correlations, the overall volatility of the portfolio is lessened. This means that even if one segment of the market experiences a downturn, other segments might perform well, cushioning the overall impact.

Asset Classes for Diversified Dividend Portfolios

Several asset classes offer dividend-paying opportunities. Including a mix of these enhances the overall portfolio resilience and return potential.

| Asset Class | Allocation Percentage | Expected Dividend Yield | Risk Level |

|---|---|---|---|

| U.S. Equities (Large-Cap) | 30% | 2-3% (Historical Average) | Moderate |

| International Equities (Developed Markets) | 20% | 2-4% (Variable by Market) | Moderate to High |

| Real Estate Investment Trusts (REITs) | 15% | 3-5% (Historically Higher) | Moderate to High |

| Fixed Income (Dividend-Paying Bonds) | 15% | 1-3% (Dependent on Interest Rates) | Low to Moderate |

| Preferred Stocks | 10% | 4-6% (Generally Higher than Common Stock) | Moderate |

| Master Limited Partnerships (MLPs) | 10% | 5-8% (High Yield, Tax Implications) | High |

Sample Diversified Dividend Portfolio

This sample portfolio illustrates diversification across sectors and geographies. Note that these are examples and the specific allocation should be tailored to individual risk tolerance and investment goals. Dividend yields and risk levels are estimates and can fluctuate. Furthermore, tax implications vary significantly based on jurisdiction and individual circumstances. Professional financial advice is recommended before making any investment decisions.

Managing and Monitoring Your Dividend Portfolio

Maintaining a thriving dividend portfolio requires diligent oversight and strategic adjustments. A passive income stream isn’t truly passive without active management; consistent monitoring ensures your investments align with your financial goals and adapt to shifting market dynamics. This involves tracking performance, analyzing dividend payouts, and making informed decisions to optimize returns and mitigate risks.Successful dividend portfolio management is a dynamic process, not a set-and-forget strategy.

Market fluctuations, company performance changes, and your own evolving financial circumstances necessitate regular review and potential adjustments. This proactive approach safeguards your investment and helps maximize your long-term passive income.

Portfolio Performance Monitoring Strategies

Effective monitoring involves a multi-faceted approach. Regularly reviewing key performance indicators provides a comprehensive understanding of your portfolio’s health and helps identify areas needing attention. This includes assessing dividend yields, payout ratios, and the overall growth of your investment. A simple spreadsheet or dedicated investment tracking software can greatly facilitate this process. Moreover, comparing your portfolio’s performance against relevant benchmarks, such as the S&P 500 dividend aristocrats index, provides valuable context and helps gauge your success relative to the broader market.

Portfolio Adjustments Based on Market Conditions and Financial Goals

Market conditions and personal financial goals are inextricably linked to portfolio management. For instance, during periods of market volatility, a shift towards more defensive dividend-paying stocks with lower risk profiles might be prudent. Conversely, a bull market might present opportunities to reinvest dividends into higher-growth companies. Similarly, life events like retirement or major purchases necessitate adjustments to your dividend income strategy, potentially requiring a change in the balance between income generation and capital appreciation.

Regularly reviewing your risk tolerance and aligning your portfolio accordingly is crucial for long-term success. For example, a younger investor with a longer time horizon might tolerate higher risk in pursuit of greater growth, while an investor nearing retirement might prioritize income stability over aggressive growth.

Dividend Income and Reinvestment Tracking

Tracking dividend income and reinvestments is essential for understanding your portfolio’s overall performance and ensuring your passive income stream grows as intended. This detailed record-keeping allows you to analyze your return on investment (ROI), assess the effectiveness of your dividend reinvestment plan (DRIP), and make data-driven decisions.

- Spreadsheet Tracking: A simple spreadsheet can effectively track dividend payments, reinvestments, and the overall growth of your investments. Columns can include the stock ticker, purchase date, cost basis, dividend payments received, reinvestment details, and current market value.

- Dedicated Investment Software: Many financial software programs and online brokerage platforms offer robust portfolio tracking features, automatically updating your holdings’ value and dividend payments. These tools often provide advanced analytical capabilities, such as performance charts and tax reporting functionalities.

- Example: Imagine an investor who receives a $100 dividend from Stock A and reinvests it to purchase additional shares. Their spreadsheet would reflect this transaction, increasing the number of shares owned and updating the cost basis accordingly. Over time, this detailed record allows the investor to monitor the growth of their investment and the cumulative effect of dividend reinvestment.

Tax Implications of Dividend Income

Dividend income, while a rewarding aspect of passive investing, carries tax implications that investors must understand to maximize their returns. The tax burden on dividends varies depending on several factors, including the investor’s tax bracket, the type of dividend (qualified or non-qualified), and the holding period of the stock. Failing to account for these factors can significantly reduce the overall profitability of your dividend investment strategy.

Dividend Tax Rates

The tax rate applied to dividend income is determined by the investor’s ordinary income tax bracket. However, a crucial distinction exists between qualified and non-qualified dividends. Qualified dividends, generally those held for more than 60 days, receive preferential tax treatment under US tax law. They are taxed at lower rates than ordinary income, mirroring the capital gains tax rates.

Non-qualified dividends, on the other hand, are taxed at the investor’s ordinary income tax rate, potentially resulting in a higher tax liability. These rates are subject to change based on federal and state tax laws, so staying informed about current regulations is crucial.

Strategies for Minimizing Dividend Tax Burden

Several strategies can help mitigate the tax burden associated with dividend income. One effective approach is to utilize tax-advantaged accounts like Roth IRAs or 401(k)s. Contributions to these accounts may be tax-deductible, and the dividend income generated within these accounts typically grows tax-free. Another strategy involves strategic tax-loss harvesting. This involves selling losing investments to offset capital gains, including those from dividend income, reducing the overall taxable income.

Finally, understanding the difference between qualified and non-qualified dividends and holding investments long enough to qualify for the preferential tax rates is paramount.

Dividend Tax Calculation Example

Let’s consider a hypothetical example. Suppose an investor in the 22% ordinary income tax bracket receives $10,000 in qualified dividends. Assuming the applicable long-term capital gains tax rate for this bracket is 15%, the tax on these dividends would be $1,500 ($10,000 x 0.15). However, if the same $10,000 were from non-qualified dividends, the tax liability would be significantly higher, at $2,200 ($10,000 x 0.22).

This illustrates the importance of understanding dividend qualifications and their impact on your overall tax liability. This example is for illustrative purposes only and does not constitute tax advice. Consult with a qualified tax professional for personalized guidance.

Risk Management in Dividend Investing

Dividend investing, while offering the potential for consistent income streams, is not without its inherent risks. Understanding these risks and implementing effective mitigation strategies is crucial for long-term success and the preservation of capital. A robust risk management framework should be a cornerstone of any dividend investing approach.

Potential Risks Associated with Dividend Investing

Several factors can negatively impact the returns from dividend investing. These risks are interconnected and their severity can vary depending on the specific investment strategy employed. Failing to account for these risks can lead to significant losses.

Mitigation Strategies for Dividend Investing Risks

Effective risk mitigation involves a multi-faceted approach encompassing diversification, thorough due diligence, and a clear understanding of your own risk tolerance. A proactive strategy, tailored to your individual circumstances, is essential.

Risk Assessment Matrix for Dividend Investment Strategies

The following matrix categorizes different dividend investing strategies based on their associated risks and provides corresponding mitigation techniques. The risk score is a subjective assessment ranging from 1 (low) to 5 (high), reflecting the potential for capital loss. This assessment is simplified and should be further refined based on individual circumstances and market conditions.

| Strategy | Potential Risks | Mitigation Techniques | Risk Score |

|---|---|---|---|

| High-Yield Dividend Stocks | Higher risk of dividend cuts or company failure; potentially overvalued stocks. | Thorough fundamental analysis; diversification across sectors and companies; focus on financially stable companies with a history of consistent dividend payments; consider using covered call options to generate income and protect against downside risk. | 4 |

| Dividend Aristocrats | Lower risk of dividend cuts but potentially slower growth compared to high-yield stocks. | Diversification within the group; regular monitoring of financial health and dividend sustainability; rebalancing portfolio periodically. | 2 |

| Dividend Growth Investing | Risk of slower initial income compared to high-yield strategies; sensitivity to economic downturns. | Long-term investment horizon; diversification across sectors and companies; focus on companies with a proven track record of dividend growth; regular monitoring of company performance and growth prospects. | 3 |

| Index Funds Focused on Dividends | Lower risk of individual stock selection errors but lower potential for outsized returns compared to active strategies. | Careful selection of index funds with a strong track record and low expense ratios; diversification provided by the index itself. | 1 |

Illustrative Example

Constructing a diversified dividend portfolio requires careful consideration of various factors, including risk tolerance, investment goals, and the current market landscape. The following example demonstrates a hypothetical portfolio allocation of $10,000, aiming for a balance between growth potential and consistent dividend income. It’s crucial to remember that past performance is not indicative of future results, and this is a simplified example for illustrative purposes only.

Individual investors should conduct thorough due diligence before making any investment decisions.This example focuses on a portfolio designed for moderate risk tolerance. The selection criteria prioritize companies with a history of consistent dividend payments, strong financial fundamentals, and reasonable valuations. Diversification is achieved through a spread across different sectors, mitigating the impact of any single company’s underperformance.

Portfolio Allocation: $10,000 Investment

The following table details the proposed allocation of a $10,000 portfolio across five different dividend-paying stocks. Dividend yields are estimates based on historical data and current market conditions, and may fluctuate. The projected annual income is a calculation based on the current dividend yield and the investment amount. It is important to note that these are projections and actual returns may vary.

| Company | Sector | Investment Amount | Shares (Approximate) | Dividend Yield (Estimate) | Projected Annual Income (Estimate) |

|---|---|---|---|---|---|

| Johnson & Johnson (JNJ) | Healthcare | $2,500 | 40 | 2.8% | $70 |

| Coca-Cola (KO) | Consumer Staples | $2,500 | 75 | 3.2% | $80 |

| Procter & Gamble (PG) | Consumer Staples | $2,000 | 45 | 2.5% | $50 |

| Verizon Communications (VZ) | Telecommunications | $2,000 | 50 | 4.5% | $90 |

| Real Estate Investment Trust (REIT)

Example Realty Income (O) |

Real Estate | $1,000 | 20 | 4.0% | $40 |

Note: The number of shares is approximate and may vary depending on the actual share price at the time of purchase. Dividend yields and projected annual income are estimates and may fluctuate due to market conditions and company performance.

Risk Considerations

Investing in dividend-paying stocks carries inherent risks. Fluctuations in the market can impact share prices, affecting both capital appreciation and dividend payouts. Company-specific risks, such as financial difficulties or changes in management, can also lead to dividend reductions or suspensions. This example portfolio aims for diversification to mitigate some of these risks, but it’s crucial to remember that no investment is entirely risk-free.

A thorough understanding of individual company financials and market trends is vital before investing.

Investing in the stock market involves risk, including the potential loss of principal. Past performance is not indicative of future results.

Ultimately, the path to passive income through dividend investing requires diligent research, strategic planning, and a long-term perspective. While inherent risks exist, a well-diversified portfolio, coupled with consistent monitoring and adjustments based on market dynamics and personal financial goals, can significantly mitigate these risks. By understanding the nuances of dividend payout ratios, tax implications, and risk management techniques, investors can harness the power of dividend investing to build a sustainable stream of passive income, fostering financial security and long-term wealth creation.

The journey may require patience and discipline, but the rewards of financial independence are well worth the effort.

Questions Often Asked

What is the difference between a dividend yield and a payout ratio?

Dividend yield represents the annual dividend per share relative to the stock’s price. The payout ratio, however, expresses the percentage of a company’s earnings paid out as dividends.

How frequently are dividends typically paid?

Dividends are typically paid quarterly, but the frequency can vary depending on the company’s policy.

Are dividends taxed?

Yes, dividends are generally subject to taxation at both the federal and state levels. The specific tax rate depends on the investor’s income bracket and the type of dividend (qualified or non-qualified).

What are the risks of investing in high-yield dividend stocks?

Companies offering extremely high dividend yields may be financially unstable or facing unsustainable business models, increasing the risk of dividend cuts or even bankruptcy.

How can I find reliable information about dividend-paying stocks?

Reputable financial websites, brokerage platforms, and company investor relations sections offer valuable information on dividend-paying stocks. It’s crucial to cross-reference data from multiple sources.

Leave a Reply